Benelux Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

Benelux Media Market Outlook

A Digitally Advanced, Multinational Ecosystem in Motion

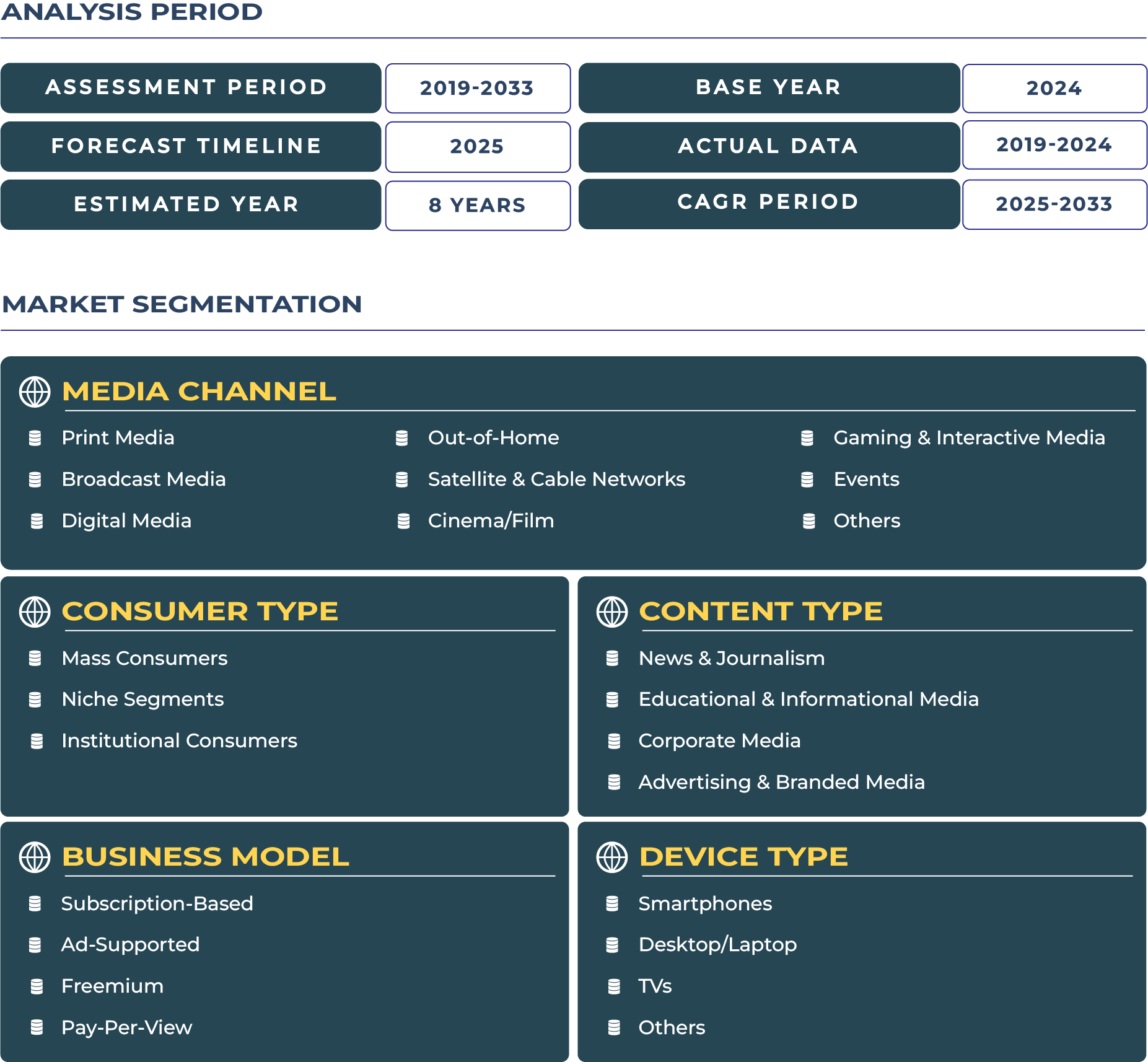

The Benelux media market—comprising Belgium, the Netherlands, and Luxembourg—stands as one of Europe's most digitally mature media ecosystems. With an estimated value of US$ XX.3 billion in 2024, the market has grown from approximately US$ XX.1 billion in 2019, showcasing a robust transformation fueled by digital acceleration, multilingual content strategies, and cross-border collaborations. According to DataCube Research, the Benelux media industry is projected to reach nearly US$ XX.6 billion by 2033, expanding at a CAGR of X.8% between 2025 and 2033. This regional cluster demonstrates a unique blend of public and private media participation, strong broadband infrastructure, and advanced consumer digital literacy. With its multilingual audiences—Dutch, French, German, and English-speaking—the Benelux media sector emphasizes cultural fluidity, cross-border appeal, and a future-ready digital infrastructure

Connectivity, Smart Devices & Policy Support Powering Media Expansion

The growth of the Benelux media ecosystem is directly linked to its widespread digital connectivity and government-led modernization programs. According to the OECD, internet penetration rates exceed 97% across all three countries, positioning Benelux among the global leaders in digital access. With a surge in smart TVs and 5G-enabled smartphones, content consumption has become seamless and platform-agnostic. In the Netherlands alone, nearly 85% of households have access to at least one video-on-demand (VoD) subscription as of 2024. Government-backed digital transformation programs like Belgium’s “Digital Belgium,” the Netherlands’ “Digital Government Strategy,” and Luxembourg’s “Media and Digital Strategy 2025” have promoted local content creation, safeguarded digital rights, and facilitated media-tech collaborations. These initiatives provide regulatory clarity and fiscal incentives that empower both legacy broadcasters and digital startups

Economic Health Underpinning Media Consumption and Advertising Growth

Economic indicators further affirm the upward trajectory of the Benelux media market. With a collective GDP per capita averaging US$ 51,000 in 2024, the region benefits from high disposable incomes, consumer readiness for premium services, and elevated advertising spend. Ad spend in the Benelux area accounts for roughly 1.05% of GDP, among the highest in Europe, highlighting the region’s mature and competitive media advertising space. Furthermore, Luxembourg’s role as a European broadcasting hub—with over 250 media and telecommunication firms registered—strengthens the region’s media exports. Dutch media content, especially formats like “Big Brother” and “The Voice,” continues to be licensed globally, reinforcing the Benelux region’s position as a content innovator and intellectual property exporter

Changing Habits: Streaming, Youth Demand & Hybrid Monetization Models

When it comes to end user behavior in Benelux, digital fluency and early tech adoption are key themes. The average Benelux consumer spends over 4.8 hours per day on media platforms, with over 70% of this engagement happening on digital screens. OTT subscriptions have seen significant growth, with over 80% penetration in the Netherlands and Belgium by 2024. Monthly digital media spending ranges between €15–30, with youth aged 18–35 leading the trend in multi-platform content consumption, gaming, and user-generated media. Despite a strong appetite for premium services like Netflix, Disney+, Videoland, and Streamz, a considerable segment still prefers freemium or ad-supported models, especially for news and sports. This dual demand is fostering innovative monetization strategies, combining subscription-based access with dynamic advertising. While medtech adoption in Benelux often drives digital health literacy, it also correlates with media trends such as wellness content, educational streaming, and interactive platforms

Brands, Platforms & Cultural Hybridity in the Benelux Media Sector

The Benelux media industry hosts a dynamic mix of global tech giants and local champions. Key domestic players include VRT (Belgium), NOS (Netherlands), RTL (Luxembourg and Belgium), and DPG Media, each playing critical roles in shaping public opinion and delivering culturally tailored content. In 2023, Belgium's Streamz—a joint venture between DPG Media and Telenet—reported over 800,000 subscribers, signaling a strong shift towards domestic streaming services. Meanwhile, Videoland, owned by RTL Netherlands, surpassed 1.3 million subscribers in 2024, boosted by local originals and cross-platform promotions. These platforms are doubling down on bilingual and multilingual content, subtitled storytelling, and genre-diverse offerings to cater to regional preferences

Strategically, Benelux media firms are focusing on co-productions with neighboring countries, AI integration in content workflows, and short-form mobile-first content to attract younger audiences. For example, in 2023, the Dutch public broadcaster NPO invested in AI-based personalization engines to tailor news and entertainment feeds across devices. Language remains a strategic consideration—Dutch, French, German, and English coexist in the media landscape, pushing broadcasters to diversify linguistically and maintain relevance across borders. This multilingual approach not only reflects demographic realities but also enhances export potential and inclusivity

Conclusion: A Digitally Native, Globally-Aware Media Future

As the Benelux media market moves toward 2033, it is poised to deepen its integration of AI, expand cross-border content collaborations, and invest in immersive formats such as AR/VR and metaverse media. The fusion of economic stability, regulatory foresight, digital access, and cultural diversity provides a strong foundation for sustainable media innovation. With end users demanding personalized, premium, and ethical content, media firms must balance technological agility with cultural depth. The Benelux media sector is not just growing—it is setting benchmarks for how small, digitally savvy regions can lead the next phase of global media transformation

Author: Joseph Gomes Y (Head – Media and Entertainment)

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation. [Learn more]

Benelux Media Market Segmentation

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

Qatar Insurance Market Size | 2019-2033

- Report ID: IAS47 | Coverage: Country |

- Category: Insurance and Securities | Sub-Category: Insurance |

- Published Date: Jul 2025 | US$495 |

South Korea PaaS Market Size | 2019-2033

- Report ID: IT1895 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Australia PaaS Market Size | 2019-2033

- Report ID: IT1896 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Malaysia PaaS Market Size | 2019-2033

- Report ID: IT1898 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Hong Kong PaaS Market Size | 2019-2033

- Report ID: IT1899 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Qatar Insurance Market Size | 2019-2033

- Report ID: IAS47 | Coverage:Country |

- Category:Insurance and Securities | Sub-Category: Insurance |

- Published Date: Jul 2025 |US$495 |

South Korea PaaS Market Size | 2019-2033

- Report ID: IT1895 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Australia PaaS Market Size | 2019-2033

- Report ID: IT1896 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Malaysia PaaS Market Size | 2019-2033

- Report ID: IT1898 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Hong Kong PaaS Market Size | 2019-2033

- Report ID: IT1899 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe