Spain Electric Vehicle Battery Market Size and Forecast by Propulsion Type, Battery Type, and Vehicle Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

Spain Electric Vehicle Battery Market Growth and Performance

- The Spain electric vehicle (EV) battery market is expected to witness strong expansion between 2025 and 2033

- Among the various segments within the Spain EV battery market, the XX segment is projected to dominate in 2025, accounting for approximately XX% of the total market share.

Spain Electric Vehicle Battery Market Outlook

Spain is carving a strategic role within the Europe electric vehicle battery supply chain, leveraging its industrial capacity and location advantages to drive long-term sustainability and innovation. The government’s ambitious PERTE VEC initiative, funded by the EU’s Next Generation recovery plan, continues to serve as the backbone of this transformation, channelling billions of euros toward domestic EV and battery infrastructure development.Spain competitive edge lies not only in its robust automotive sector, which contributes nearly 10% to the national GDP, but also in its commitment to building an integrated battery value chain. The €10 billion investment by Volkswagen and SEAT to electrify Spain’s automotive industry further exemplifies this vision. This investment supports new EV production facilities and battery manufacturing expansions, propelling Spain into the spotlight as a European hub for electric mobility.

In addition, initiatives by regional governments are complementing national strategies. The Government of Catalonia, for example, launched its Electric Vehicle Promotion Plan 2025–2030, committing over €1.4 billion to EV infrastructure and supply chain development. With renewable-powered gigafactories and cross-border trade opportunities via its geographical positioning, the Spain Electric Vehicle Battery Market is on a resilient growth path, backed by cohesive public-private collaboration. ?

Spain Electric Vehicle Battery Market Drivers

Spain electric vehicle battery sector is advancing rapidly, fuelled by targeted industrial policies, landmark investments in gigafactories, and rising regional demand for localized battery supply chains. The most prominent is the multi-billion-euro public investment led by the Spanish government through the PERTE VEC program, designed to attract battery-related investments and accelerate the electrification of Spain's automotive sector. Complementing this, the European Commission’s push for a local, circular battery economy is incentivizing domestic production and recycling capabilities.One of the major foreign direct investments catalysing this momentum is the recently announced €4.1 billion joint venture between Stellantis and China’s CATL to build a battery plant in Zaragoza. With a production target of 50 GWh by 2026—enough to power approximately 700,000 vehicles per day—the plant will focus on lithium iron phosphate batteries for small to medium EVs. The venture capitalizes on Spain’s competitive energy and labour costs, as well as government subsidies, underlining the country’s increasing attractiveness as a battery production destination.

Market dynamics are further shaped by rising consumer demand for EVs and growing expectations for sustainable, localized supply chains. These elements collectively accelerate the localization of raw material sourcing, component manufacturing, and battery assembly within Spain, fortifying the Spain Electric Vehicle Battery Industry against external shocks and global supply disruptions.

Spain Electric Vehicle Battery Industry Trends

Spain’s battery sector is undergoing dynamic shifts as it transitions from policy-driven planning to execution-focused industry deployment. The gigafactory model is central to this evolution, with facilities like PowerCo’s Sagunto plant and Stellantis-CATL’s Zaragoza factory set to transform the industrial landscape. Both factories will operate on renewable energy, reflecting Spain’s broader sustainability objectives and aligning with EU taxonomy requirements. The strategic use of second-life batteries in grid stabilization and stationary energy storage projects. Spanish startups and research institutions are actively pioneering solutions in this area, promoting a closed-loop system within the Spain Electric Vehicle Battery Market. These efforts complement Spain’s expanding solar and wind capacity, allowing the reuse of EV batteries as grid-scale assets.

Innovation in battery chemistry is also accelerating. Institutions like the Institute of Molecular Science (ICMol) and CIC energiGUNE are spearheading R&D into solid-state and next-gen lithium batteries. According to CIC energiGUNE, projections from 2021 estimated Spain’s annual battery demand could reach 75 GWh by 2030, prompting government and industry to establish two to three large-scale gigafactories. The emergence of private-public consortiums and dedicated innovation clusters marks Spain's commitment to long-term R&D competitiveness. Digital transformation remains integral, with AI-enabled battery monitoring, lifecycle forecasting, and supply chain digitalization gaining traction across leading battery firms and OEMs operating in Spain. ?

Spain Electric Vehicle Battery Industry Development

The Spain Electric Vehicle Battery Market has undergone a transformative phase in recent years, shaped by a convergence of strategic investments, public-private initiatives, and evolving industrial policies aimed at strengthening its role within Europe’s green mobility shift. One of the most prominent milestones came in July 2023, when Volkswagen’s battery subsidiary, PowerCo, broke ground on its €10 billion gigafactory in Sagunto, Valencia. This project, supported by Spain’s PERTE VEC funding program, marks a foundational step toward creating a self-sufficient EV battery supply chain in Spain. Once operational, the facility is projected to produce up to 40 GWh of battery capacity annually, supplying cells for Volkswagen’s expanding fleet of electric vehicles manufactured domestically.

In a parallel push to build regional manufacturing strength, Envision AESC revealed plans in June 2023 to establish a €2.5 billion gigafactory in Navalmoral de la Mata, Extremadura. The plant, designed to deliver 30 GWh of annual output, aims to serve leading European automakers while generating around 3,000 jobs. This development aligns with Spain's goal to attract foreign direct investment into high-tech, job-creating sectors. Also, Spain's aspirations are not limited to conventional lithium-ion technology. In the Basque Country, Basquevolt has emerged as a national leader in next-generation battery innovation. Backed by over €70 million in funding by early 2024, the consortium began producing pilot solid-state cells in 2025 and is targeting full-scale industrial production by 2027. This focus on solid-state R&D is positioning Spain as a competitive player in future-proof battery technologies.

Collaboration within Europe is further reflected in strategic partnerships like the one between Slovak battery innovator Inobat and Spain’s QEV Technologies. In 2024, the two companies signed an agreement to jointly develop and assemble battery modules at QEV’s Montmeló facility near Barcelona. The project is tailored to electrify commercial fleets and strengthens Spain’s role in providing integrated battery solutions across multiple transport segments.

Meanwhile, the Automotive Cells Company (ACC)—a high-profile joint venture formed by Stellantis, Mercedes-Benz, and TotalEnergies—has been assessing Spain as a potential host country for future gigafactory expansion. Although a final decision has not yet been made, ACC’s interest reflects growing confidence in Spain’s supportive industrial ecosystem, labour market, and infrastructure readiness for large-scale battery manufacturing.

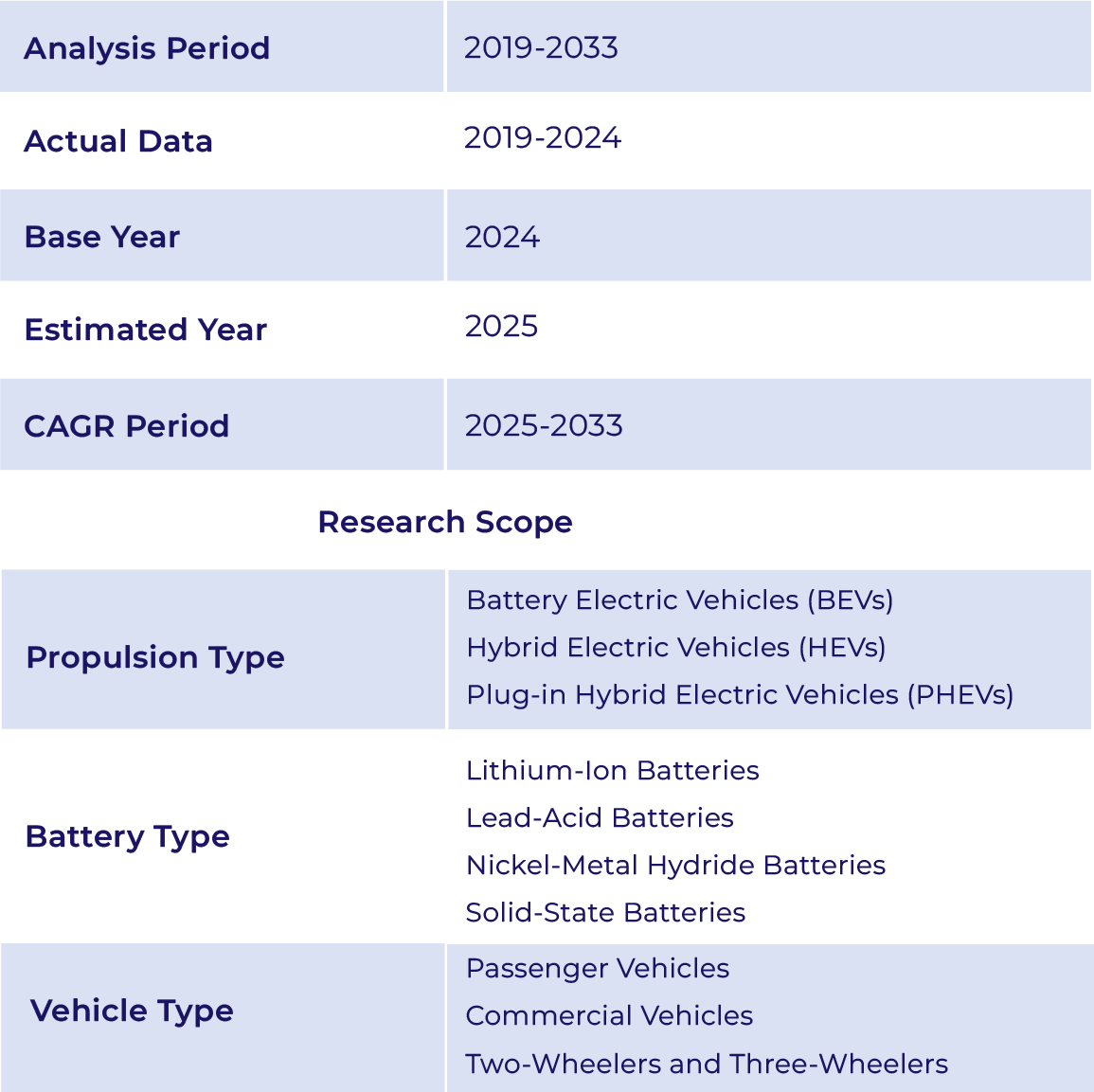

Spain Electric Vehicle Battery Market Scope

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

UAE Public Cloud Market Size | 2019-2033

- Report ID: IT1799 | Coverage: Country |

- Category: Information Technology | Sub-Category: IT Software & Services |

- Published Date: Jul 2025 | US$495 |

Indonesia Drone Detection System Market Size | 2019-2033

- Report ID: A&D63 | Coverage: Country |

- Category: Aerospace & Defence | Sub-Category: Defence |

- Published Date: Jul 2025 | US$495 |

UAE Public Cloud Market Size | 2019-2033

- Report ID: IT1799 | Coverage:Country |

- Category:Information Technology | Sub-Category: IT Software & Services |

- Published Date: Jul 2025 |US$495 |

Indonesia Drone Detection System Market Size | 2019-2033

- Report ID: A&D63 | Coverage:Country |

- Category:Aerospace & Defence | Sub-Category: Defence |

- Published Date: Jul 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe