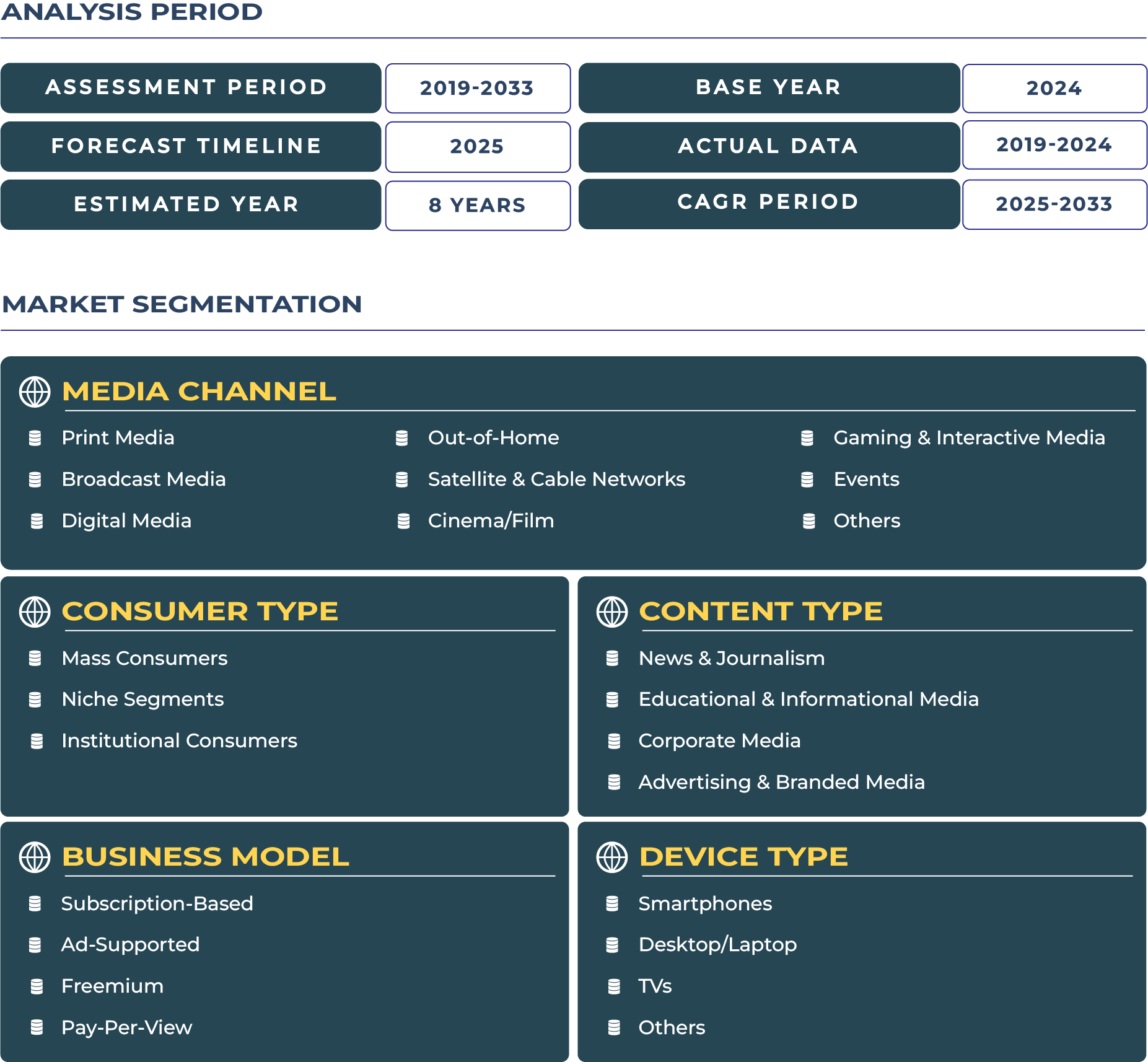

India Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

India Media Market Growth and Performance

- India media market size is expected to witness substantial growth in the coming years, expanding at a CAGR of XX.56% to achieve market value of US$ XX.5 billion by 2033.

- The media industry in India stood at US$ XX.9 billion in 2024.

India Media Industry Outlook

A Flourishing Media Ecosystem Driven by Digital Acceleration

The India media industry ecosystem is undergoing a transformative phase, propelled by rising internet access, surging smartphone penetration, and increasing digital consumption. In 2023, the India media market witnessed unprecedented growth with over 700 million internet users and smartphone ownership surpassing 600 million, laying the foundation for a hyper-connected consumer base. Moving into 2024 and beyond, the sector is expected to see continued momentum with a sharp focus on regional content, vernacular engagement, and next-gen digital platforms. Backed by massive investments in digital infrastructure and government support under the Digital India initiative, the India media sector is projected to emerge as one of the top global media markets within the next five years.

Role of Economic Indicators in Shaping Media Growth

India’s rising GDP per capita and expanding disposable income are playing a pivotal role in media market expansion. In 2023, GDP per capita reached US$ 2,600 with a projected annual growth rate of 6-7%. This economic upswing translates into greater willingness among consumers to pay for premium content, paving the way for monetization models beyond traditional ad revenues. Currently, advertising spends constitute about 0.3% of GDP, and this figure is expected to climb to 0.4% by 2025, buoyed by the explosive growth in digital advertising. As India's middle class expands and premium content offerings rise, brands are aggressively allocating budgets toward programmatic, influencer-driven, and regional ad campaigns—reshaping revenue models across the India media industry.

Consumer Preferences and Demographics Redefining Media Dynamics

Consumer behavior in India is evolving rapidly, with viewers averaging four hours of daily media consumption. The shift from traditional TV to on-demand and mobile-first platforms is most noticeable among urban and semi-urban youth. A staggering 65% of India’s population is under the age of 35, making it a hotspot for youth-centric content, especially in the genres of drama, sports, reality, and music. Consumer preference is gradually moving from freemium models to premium subscriptions, supported by increased spending power. While price sensitivity remains a factor, especially in tier-2 and tier-3 cities, there’s growing appetite for ad-free experiences and exclusive shows on platforms like Netflix, Amazon Prime Video, Disney+ Hotstar, SonyLIV, and Zee5. The average media spend per user currently stands at US$ 3.60 per month, with projections indicating a gradual rise as value-driven content expands.

Digital Channels and Content Personalization: Key Growth Drivers

The India media industry is no longer television-first. OTT (Over-the-top) platforms have seen meteoric growth, with subscriber bases reaching around 100 million in 2023 and expected to grow by 20% in 2024. By 2025, OTT penetration is projected to hit 150 million, driven by cheaper data plans, low-cost smartphones, and regional language content. Personalized recommendations, AI-driven user experiences, and on-the-go mobile consumption are central to the success of these platforms. Major players like Reliance Jio and Bharti Airtel are strategically bundling OTT subscriptions with telecom services, making premium content accessible to a broader population.

Additionally, smart TV adoption is rising steadily, especially in non-metro cities, offering new avenues for hybrid viewing that merges linear TV with app-based platforms. With government initiatives fostering local content creation and liberalized FDI norms in media, the environment is ripe for both international giants and local players to scale operations.

Brand Strategies and Customer Acquisition: A Competitive Outlook

Top media brands, both domestic and global, are deploying multi-channel strategies to capture India's diverse audience. Disney+ Hotstar, for example, has heavily invested in IPL cricket streaming to hook both free and paid users, while Zee5 is enhancing its regional content library to build deeper cultural resonance. Meanwhile, Amazon Prime Video and Netflix continue to experiment with mobile-only plans and regional dubbing to increase their reach. Local giants like Reliance JioCinema are reshaping the game by offering blockbuster content for free under their telecom ecosystems, rapidly scaling their user base. Customer acquisition strategies now revolve around data bundling, AI-based engagement, vernacular personalization, and flexible subscription models—ushering in a new era of intelligent media delivery in the India media sector.

India Media Market Scope

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

China Media Market Size | 2019-2033

- Report ID: MED512 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

South Korea Media Market Size | 2019-2033

- Report ID: MED513 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

China Media Market Size | 2019-2033

- Report ID: MED512 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

South Korea Media Market Size | 2019-2033

- Report ID: MED513 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe