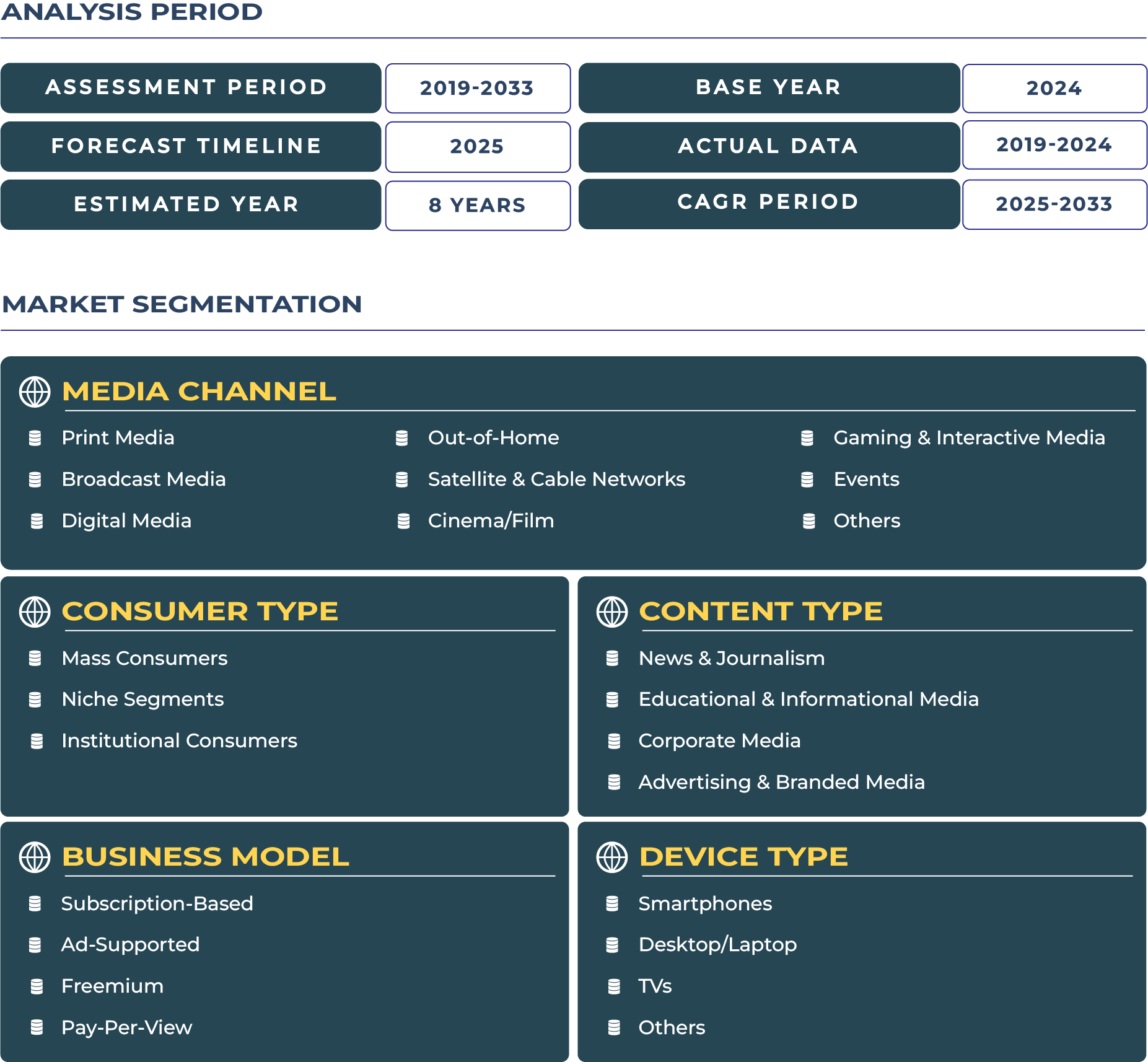

South Korea Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

South Korea Media Market Growth and Performance

- It's evident that the South Korea media market size is on track to reach an impressive US$ XX.12 billion in revenue by 2025.

- This growth trajectory is underpinned by an expected Compound Annual Growth Rate (CAGR) of X.92% from 2025 to 2033, as forecasted by DataCube Research.

South Korea Media Industry Outlook

Global Influence Rooted in Local Innovation

The South Korea media industry is not just a regional powerhouse—it’s a global cultural force. Propelled by the Korean Wave or Hallyu, which continues to gain momentum across continents, the sector is undergoing rapid digital transformation. In 2023, the industry witnessed robust growth through international content distribution, particularly in K-dramas, K-pop, and webtoons, backed by OTT platforms such as Netflix Korea, Wavve, and Tving. As South Korea's media sector ventures into 2024 and beyond, the fusion of government-backed innovation (through initiatives like the Digital New Deal) and AI-driven content strategies is setting the stage for unprecedented evolution in content delivery, monetization, and global reach. Digital ecosystems are becoming central to storytelling, offering rich user experiences across mobile, smart TVs, and cross-platform integrations.

Market Drivers

The South Korea media market is deeply shaped by its economic indicators. With a GDP per capita of USD 34,757 and disposable income averaging USD 23,000 per individual (2023), South Korean households are financially empowered to invest in premium media experiences. This spending capacity translates directly into the digital content economy, where consumer willingness to pay for high-quality, ad-free, localized K-content is notably high. Advertising spend in 2023 reached USD 13.2 billion, accounting for 0.7% of GDP, with digital ads commanding over 55% share, primarily across mobile and OTT platforms. Programmatic advertising, influencer-led marketing, and mobile video content are now central to brand engagement strategies, creating a dynamic interplay between consumer behavior and monetization models.

Demographic Pulse: Youth-Driven Content Evolution

Youth demographics—particularly those aged 15–34, comprising 24% of South Korea’s population—are central to the media industry’s evolution. These 12.5 million digital natives contribute significantly to media revenues, spending USD 19–30 monthly on streaming, fandom subscriptions, webtoons, and exclusive interactive content. Their preferences are rapidly shaping industry norms: from K-pop fandom ecosystems and live-streamed concerts to choose-your-own-ending dramas and gamified webtoons. The tech-savvy nature of this demographic also leads to dual-screening behavior, with users actively engaging with mobile and TV simultaneously, especially during 6–10 PM peak hours. This trend has led platforms to adopt real-time interactivity, gamification, and AI-personalized feeds to sustain engagement.

Media Habits, OTT Penetration, and Channel Preferences

In 2023, South Koreans averaged 6.2 hours of media consumption daily, with YouTube (44+ million monthly users), Naver TV, Netflix Korea (5.2M subscribers), and KakaoTV leading the content consumption curve. OTT platform penetration reached 73% of households, with an average of 1.6 subscriptions per household and monthly spend ranging between USD 9–13. Consumers increasingly prefer ad-free, binge-worthy formats, localized subtitles, and immersive audio-visual experiences. While Naver and Kakao dominate with regional language and user-generated content, global platforms like Netflix continue investing in local productions, such as its blockbuster partnerships with Studio Dragon.

Strategic Moves by Media Titans: Differentiation in a Crowded Space

Key players in the South Korea media sector are deploying nuanced strategies to expand user base and content IP. CJ ENM, for instance, fortified its position by merging Tving with KT Seezn in 2022, creating a super-platform with wide content variety and AI-curated personalization. Netflix Korea, on the other hand, has doubled down on local production with shows like The Glory and Kingdom, while also co-producing globally exportable K-dramas. Naver Webtoon has evolved into a global storytelling giant, integrating comics with video content and creator tools powered by AI. Meanwhile, Kakao M is building transmedia ecosystems—transforming webtoon IPs into dramas and integrating fan-driven commerce.

Each player’s go-to-market strategy hinges on three core pillars: IP differentiation, cross-platform engagement, and global expansion through localized narratives. These strategic imperatives enable them to secure long-term user loyalty and increase the lifetime value per subscriber.

The Role of Policy in Powering a Digital Content Economy

Government regulations are acting as catalysts in the digital transformation of the South Korea media industry. The Digital New Deal, a USD 43.5 billion initiative (KRW 58.2 trillion), is aimed at nurturing cloud platforms, AI tools, and digital content creators. Projects like Content Korea Lab and KOCCA offer financial support to indie creators and startups in gaming and animation, while the OTT Support Bill (2023) is designed to foster fair competition, localization, and digital rights protection. These efforts are not just regulatory—they’re strategic, providing South Korea’s creative economy with the momentum needed to scale globally while protecting local innovation.

South Korea Media Market Scope

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

UK Public Cloud Market Size | 2019-2033

- Report ID: IT1811 | Coverage: Country |

- Category: Information Technology | Sub-Category: IT Software & Services |

- Published Date: Jul 2025 | US$495 |

Germany Public Cloud Market Size | 2019-2033

- Report ID: IT1812 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Jul 2025 | US$495 |

UK Public Cloud Market Size | 2019-2033

- Report ID: IT1811 | Coverage:Country |

- Category:Information Technology | Sub-Category: IT Software & Services |

- Published Date: Jul 2025 |US$495 |

Germany Public Cloud Market Size | 2019-2033

- Report ID: IT1812 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Jul 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe