Israel Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

Isreal Media Market Outlook

A Mature but Agile Media Market

The Israel media market is undergoing a compelling transformation marked by technological innovation, high digital adoption, and evolving content consumption patterns. As of 2024, the market is estimated to be valued at approximately US$ XX.1 billion and is expected to reach nearly US$ XX.3 billion by 2033, growing at a CAGR of XX.8% during 2025–2033, according to insights from DataCube Research. The Israel media industry encompasses diverse verticals including television broadcasting, OTT streaming, digital publishing, print media, audio streaming, and online gaming—each showing varying levels of digital maturity and consumer adoption

The Israel media sector is also distinguished by its resilience and ability to adapt swiftly to political, economic, and technological changes. Traditional TV still holds relevance, but streaming services and social media platforms have aggressively penetrated the market, redefining how content is created and consumed. The presence of multilingual audiences—Hebrew, Arabic, English, and Russian speakers—also adds complexity to content strategies, making localization a core driver for platform growth. Israel’s media evolution is no longer just linear but hyperconnected, personalized, and algorithm-driven

Digital Foundations Fueling Growth: Drivers, Innovation & Regulatory Boost

The robust growth of the Israel media ecosystem is fundamentally powered by digital enablers. With over 91% internet penetration as of 2023 and nearly 6 million smartphone users, the nation boasts one of the highest digital literacy rates in the Middle East. This infrastructure enables seamless access to a wide range of media formats—especially OTT, mobile news apps, video-on-demand, and social platforms. Popular OTT platforms like Netflix, Apple TV+, and local players such as Yes+ and Cellcom TV are consistently gaining traction

Government-led digitization strategies are also helping shape the industry. The Israeli Ministry of Communications has implemented reforms to liberalize content broadcasting and enhance fair competition. In 2024, Israel announced plans to regulate digital advertising standards and OTT content licensing, promoting transparency and consumer protection while attracting global players to invest in local operations. Moreover, Israel’s Innovation Authority continues to fund startups and R&D labs that explore AI-driven content generation, smart adtech, and interactive formats like AR/VR storytelling. These structural supports are accelerating innovation and pushing Israel’s media industry into a new era of growth

Economic Tailwinds: Rising GDP, Exports & Ad Spend Catalyze Market Expansion

The Israeli economy’s resilience is another cornerstone of media market expansion. With a GDP per capita of approximately US$ 52,000 in 2024 and an average household disposable income of over US$ 36,000, Israeli consumers are increasingly inclined to pay for premium content. Moreover, advertising expenditure now accounts for around 0.9% of GDP, and is steadily rising, led by sectors like fintech, ecommerce, and edtech

Media imports—such as global films, syndicated shows, and OTT licenses—still dominate overall content flow, but local media exports are catching up. Israeli TV formats such as Fauda, Tehran, and Shtisel have found significant international acclaim, opening new monetization channels through Netflix, Hulu, and BBC collaborations. This export trajectory not only enhances revenue generation but also elevates Israel’s soft power in global media diplomacy

Demographics & Media Adoption Trends in Israel

End user behavior in Israel is clearly gravitating toward digital-first experiences. On average, Israelis spend over 7.5 hours daily engaging with media, a number that continues to climb among the younger population. Video streaming and online news top the charts, followed by social networking, audio streaming, and casual gaming. The high smartphone penetration rate (estimated at 85% in 2024) and smart TV ownership (70% of households) are key enablers of this consumption shift

OTT subscription penetration is now above 63% of households, and youth (aged 18–34) comprise the most active consumer group, accounting for over 40% of total digital media consumption. This demographic also exhibits a strong preference for interactive and user-generated content platforms like TikTok, YouTube, and Twitch. While price sensitivity is a concern in rural segments, urban users show a strong affinity for premium and ad-free media services. This trend suggests growing market stratification based on economic profiles and digital maturity

Brands, Platforms & Partnerships in Motion

Israel is home to a diverse array of media brands that include both global names and local champions. Among broadcasters, KAN (Israel Public Broadcasting Corporation), Reshet 13, and Keshet 12 dominate the traditional segment, while Yes+, HOT, and Cellcom TV lead the OTT and IPTV markets. Globally active platforms like Netflix, Amazon Prime Video, and Disney+ have customized their offerings for Israeli audiences through Hebrew subtitles, regional pricing, and culturally relevant content. As of early 2024, Netflix had an estimated 1.2 million subscribers in Israel, reflecting its local foothold

Strategically, media companies are adopting multi-channel engagement strategies. Keshet’s launch of MakoTV in 2023, a hybrid streaming app that offers both live and on-demand content, is an example of this dual approach. HOT partnered with Paramount Global in 2024 to co-produce original mini-series for both Israeli and U.S. markets, tapping into cross-border monetization. Additionally, Spotify and Apple Music are investing in localized audio content, including podcasts and exclusive releases in Hebrew and Arabic, enhancing content stickiness among young users

Promotional strategies now revolve around influencer collaborations, content gamification, and cross-platform bundling with telecom and broadband services. Partnerships between Bezeq and major OTT players have introduced bundled subscriptions at discounted rates, encouraging paid adoption across platforms. This convergence of telecom, entertainment, and adtech underscores the emerging trend of platform-based ecosystems

Author:

Joseph Gomes Y (Head – Media and Entertainment)

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation. [Learn more]

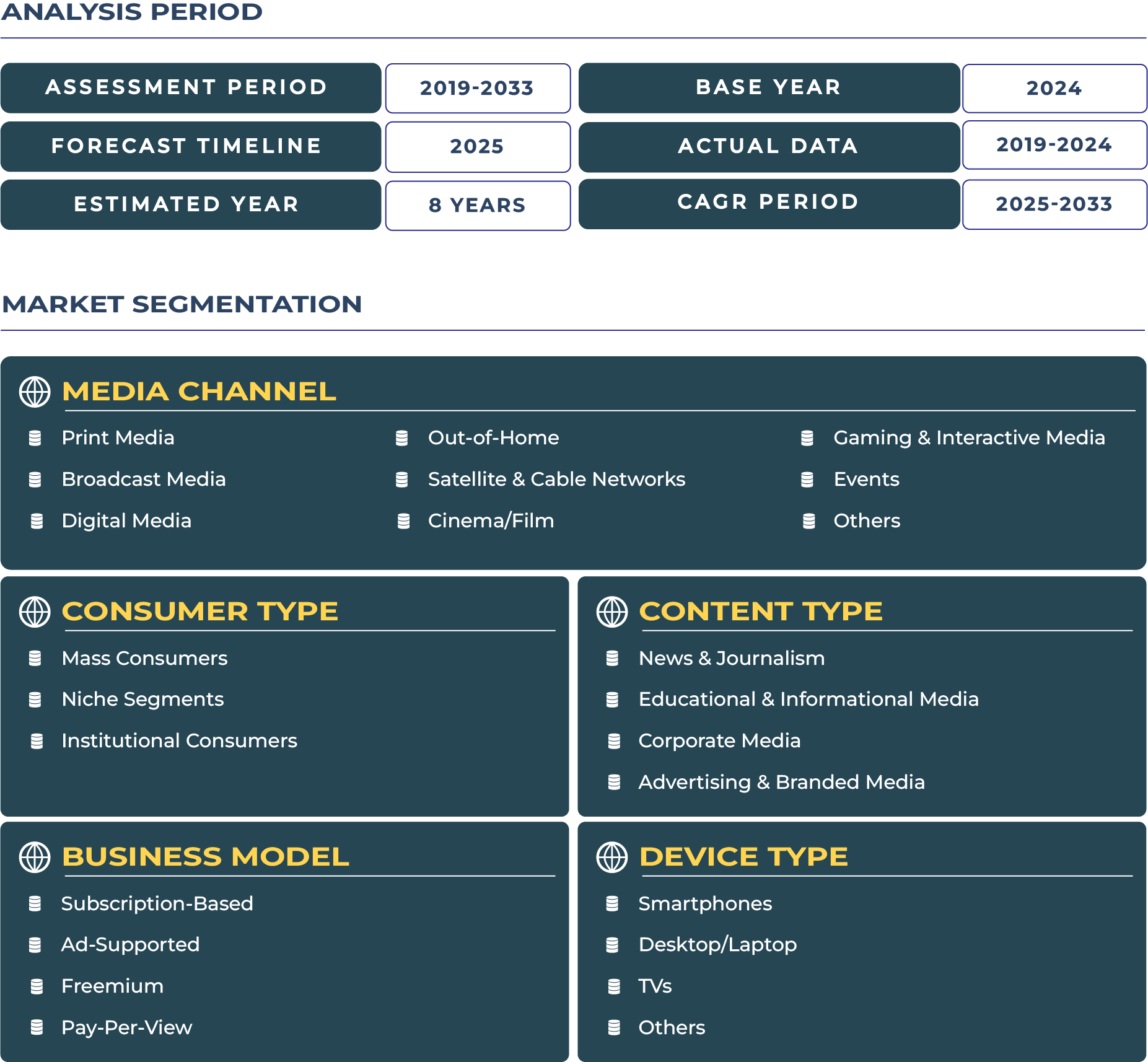

Isreal Media Market Segmentation

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

India Media Market Size | 2019-2033

- Report ID: MED511 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

Asia Pacific Media Market Size | 2019-2033

- Report ID: MED5116 | Coverage: Regional |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$1,345 |

Saudi Arabia Media Market Size | 2019-2033

- Report ID: MED5141 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

UAE Media Market Size | 2019-2033

- Report ID: MED5146 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

GCC Media Market Size | 2019-2033

- Report ID: MED5147 | Coverage: Regional |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$1,345 |

India Media Market Size | 2019-2033

- Report ID: MED511 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

Asia Pacific Media Market Size | 2019-2033

- Report ID: MED5116 | Coverage:Regional |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$1,345 |

Saudi Arabia Media Market Size | 2019-2033

- Report ID: MED5141 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

UAE Media Market Size | 2019-2033

- Report ID: MED5146 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

GCC Media Market Size | 2019-2033

- Report ID: MED5147 | Coverage:Regional |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$1,345 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe