Nordics Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

Nordics Media Market Outlook

The Nordics media market—comprising Sweden, Norway, Denmark, Finland, and Iceland—has evolved into a robust, digitally empowered ecosystem, backed by strong infrastructure, digital literacy, and high-income populations. Between 2019 and 2024, the market exhibited steady digital transformation with a compound annual growth of nearly 6.7%, primarily driven by digital media services, OTT platforms, and hybrid content consumption models. As we look ahead from 2025 to 2033, the market is poised for further expansion at a projected CAGR of X.9%, propelled by content personalization, AI-driven content delivery, and 5G infrastructure. According to DataCube Research, the market valuation is expected to surpass US$ XX.5 billion by 2033, up from approximately US$ XX.1 billion in 2024. The Nordics media sector is now positioned as a global model for digital-first content ecosystems, where media convergence and cross-platform storytelling dominate consumer engagement

Innovation, Infrastructure & Policy: Accelerating Media Momentum

The explosive rise of smart TVs, 5G connectivity, and mobile media platforms has empowered the Nordics media industry with unparalleled content delivery efficiency. As of 2024, the region boasts an average internet penetration of 97%, with countries like Norway and Sweden nearing saturation levels. This widespread connectivity supports the rapid adoption of streaming services, mobile-first news platforms, and immersive experiences such as AR-enhanced media. Nordic regulators have also laid down progressive policies like Finland’s Digital Strategy 2030 and Denmark’s Media Agreement 2023–2026, ensuring fair access to digital infrastructure and promoting local content creators. Meanwhile, Norway’s NRK and Sweden’s SVT continue to invest in AI-powered personalization engines, enhancing user engagement and setting benchmarks for the Nordics media ecosystem. Government-backed digital literacy programs further encourage elderly and rural populations to access news and entertainment platforms, deepening user penetration across age groups

Wealth, Trade & Spending: The Economics of Nordic Media

From 2019 to 2023, robust macroeconomic indicators such as high GDP per capita (averaging over US$ 60,000 in Norway and Denmark) and disposable incomes have fueled consumer spending on media subscriptions and digital services. The advertising spend as a percentage of GDP in the region consistently hovers around 1.5%, significantly above the EU average, indicating strong brand investment in content platforms. The Nordics media sector also benefits from a flourishing media export ecosystem—particularly in Sweden and Denmark—where homegrown dramas, documentaries, and music productions find markets in North America, Asia, and Europe. Media imports, especially from the US and UK, continue to shape consumer tastes, but there’s a growing emphasis on culturally contextual content created by local talent and supported by state grants and export agencies

The Content-Hungry Consumer: Youth-Led Adoption Trends

Nordic audiences are among the most engaged media consumers globally, with average daily media consumption nearing 6.4 hours per day as of 2024, including digital, print, and audiovisual content. OTT platforms enjoy a penetration rate of over 78%, driven predominantly by Gen Z and millennials, who prioritize on-demand content, short-form videos, and localized genres. Premium subscriptions dominate—over 65% of OTT users in Sweden, for instance, subscribe to ad-free models, indicating a growing willingness to pay for quality. This is partly due to the higher purchasing power and digital maturity of end users. However, price sensitivity still persists among the older demographic and in rural pockets. According to DataCube Research, end user behavior in Nordics showcases a dual trend—while urban youth are inclined towards AI-personalized content and multi-platform usage, rural users prefer simplified access via national broadcasters. Meanwhile, the medtech adoption in Nordics has spurred parallel growth in health media content, particularly around telehealth, fitness, and mental well-being storytelling formats

From Global Giants to Local Heroes: Brand Wars and Strategy Playbooks

The Nordics media ecosystem hosts a powerful mix of global streaming giants and local innovators. Netflix, HBO Max, and Disney+ maintain significant subscriber bases—Netflix alone commands nearly 2.3 million subscribers in Sweden as of 2024. However, regional players like Viaplay, DR TV (Denmark), and Yle Areena (Finland) are rapidly catching up with hyperlocal strategies, regional content, and strategic alliances. For instance, in March 2024, Viaplay entered a co-production deal with Norwegian studio Motion Blur to develop Scandi-noir thrillers tailored for both local and international markets

Language and cultural relevance remain critical to strategy. Local platforms increasingly prioritize Nordic languages and folklore-based storytelling to enhance cultural resonance. Spotify, originally from Sweden, leads the audio streaming category with hyper-targeted regional podcasts and cross-platform media integrations. Additionally, media companies are integrating AI to optimize scheduling, user recommendations, and predictive analytics. SVT, for example, introduced a deep-learning-based news aggregator in early 2025, boosting user engagement by over 18% in three months

Final Thoughts: Where Innovation Meets Identity

The Nordics media market stands as a blueprint for next-gen content ecosystems—where innovation, cultural authenticity, and high user engagement converge. With government backing, affluent demographics, and a strong export culture, the region is poised to set global trends in immersive, inclusive, and intelligent media experiences. As 2033 approaches, expect further convergence across platforms, a rise in AI-powered media personalization, and a continued balancing act between global content appeal and Nordic cultural identity

Author: Joseph Gomes Y (Head – Media and Entertainment)

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation. [Learn more]

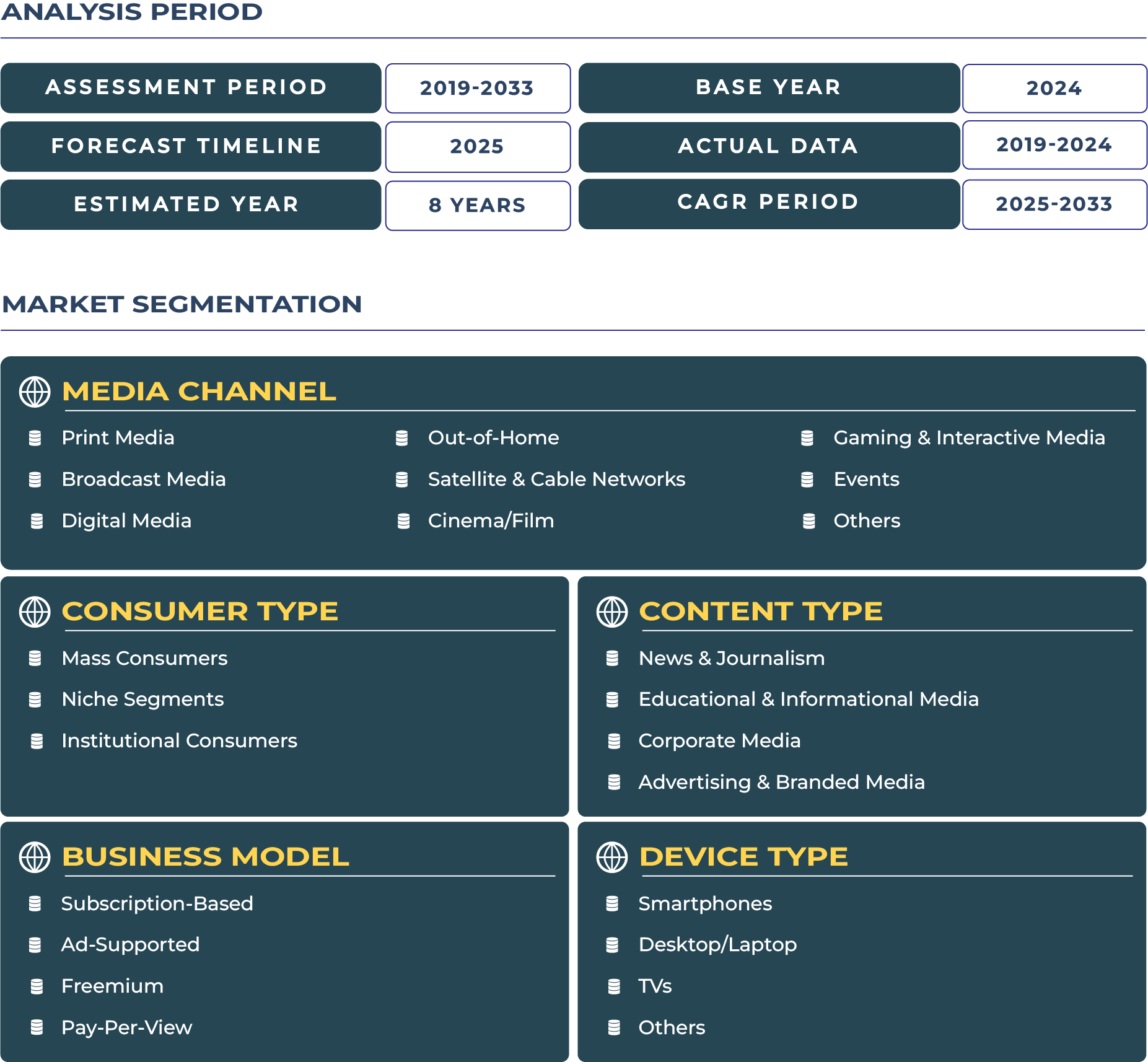

Nordics Media Market Segmentation

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

Qatar Insurance Market Size | 2019-2033

- Report ID: IAS47 | Coverage: Country |

- Category: Insurance and Securities | Sub-Category: Insurance |

- Published Date: Jul 2025 | US$495 |

South Korea PaaS Market Size | 2019-2033

- Report ID: IT1895 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Malaysia PaaS Market Size | 2019-2033

- Report ID: IT1898 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Indonesia PaaS Market Size | 2019-2033

- Report ID: IT1900 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 | US$495 |

Qatar Insurance Market Size | 2019-2033

- Report ID: IAS47 | Coverage:Country |

- Category:Insurance and Securities | Sub-Category: Insurance |

- Published Date: Jul 2025 |US$495 |

South Korea PaaS Market Size | 2019-2033

- Report ID: IT1895 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Malaysia PaaS Market Size | 2019-2033

- Report ID: IT1898 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Indonesia PaaS Market Size | 2019-2033

- Report ID: IT1900 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Dec 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe