Qatar Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

Qatar Media Market Outlook

The Rise of a Regional Media Hub

The Qatar media market is emerging as a formidable force in the MENA media ecosystem, backed by visionary investments, cutting-edge infrastructure, and a rapidly digitizing population. Between 2019 and 2024, the media industry in Qatar saw a consistent CAGR of around X.2%, with the pace expected to accelerate to X.4% between 2025 and 2033, according to revised estimates from DataCube Research. By 2033, the market is projected to reach US$ XX.6 billion, driven by expanding digital content platforms, innovative broadcasting models, and Qatar’s ambition to become a regional content creation hub

Key media sectors such as television broadcasting, digital advertising, OTT streaming, and sports media are showing double-digit growth. Al Jazeera remains the flagship of the Qatar media industry, maintaining global relevance in news reporting while diversifying into digital formats. Simultaneously, state-backed initiatives are promoting Arabic-language content and pushing media innovation aligned with national identity. Qatar’s successful hosting of the FIFA World Cup 2022 served as a catalyst, bringing global attention to its media capabilities and infrastructure. The country now boasts some of the most advanced studios and satellite networks in the region

Drivers of Growth: Digital Innovation and Regulatory Foresight Fueling Expansion

The Qatar media sector is witnessing an upsurge in digital content consumption fueled by robust internet penetration of 99.6% (as of 2024) and one of the highest mobile broadband subscription rates per capita globally. The demand for smartphones, 5G services, and smart TVs is enabling seamless access to streaming platforms, news apps, and interactive content formats. According to GSMA Intelligence, over 95% of Qataris own internet-enabled smartphones, creating a strong user base for mobile-first content

Government support has been instrumental in accelerating media digitization. The Qatar National Vision 2030 outlines a clear objective to enhance cultural representation and digital media exports, and the Ministry of Culture has actively funded production studios and training programs in partnership with regional players. In 2023, the launch of Qatar Media City (QMC)—a free zone designed to attract global and regional media companies—marked a strategic move to localize content production and incubate media startups

In terms of regulation, the Communications Regulatory Authority (CRA) has worked to ensure fair competition, content moderation, and quality standards across digital and traditional media. With updated guidelines on streaming services and advertising disclosures released in 2024, Qatar is fostering a transparent and future-ready media environment. This alignment of infrastructure, policy, and consumer behavior is central to the country’s media success story

Balancing Growth and Caution: Economic and Structural Challenges

Despite the growth momentum, the Qatar media market faces notable challenges that could temper its long-term trajectory. One significant concern is the concentration of media ownership and limited diversity in editorial voices. While this ensures quality control and centralized strategy, it also hinders the development of independent media voices that can enrich the content ecosystem

On the economic front, although Qatar has one of the highest GDP per capita globally (USD 84,000+ as per IMF 2024), advertising spend remains relatively conservative. In 2024, advertising expenditure accounted for just 0.65% of GDP, indicating potential underutilization of media channels for brand storytelling. Additionally, language barriers—predominantly Arabic and English content—create friction for more inclusive media engagement among South Asian and East African communities residing in Qatar

The market is also susceptible to global shifts, such as streaming platform saturation and rising content acquisition costs. With international players like Netflix, Amazon Prime, and Disney+ vying for local attention, domestic platforms may find it challenging to scale without significant capital or regional alliances. These factors necessitate a balanced, innovation-led approach to sustain media expansion in the long run

The Digital Consumer: Multi-Device, Multi-Platform, and Hyper-Engaged

Consumer behavior is at the heart of Qatar’s media transformation. The average Qatari consumer spends around 8.7 hours daily on media consumption, with 4.1 hours on mobile devices, according to a 2024 study by DataCube Research. Digital platforms now surpass traditional TV in viewership, with YouTube, Shahid, Netflix, and TikTok among the most consumed platforms. Interestingly, OTT penetration stands at 59%, with the average subscriber spending QAR 45–60 monthly on streaming services

A youthful, cosmopolitan demographic fuels this demand. Over 55% of the population is under the age of 35, and a significant portion comprises tech-savvy expatriates who prefer global content, esports, and interactive news formats. These consumers are increasingly choosing on-demand, personalized content experiences over passive media consumption

From an economic standpoint, Qatar’s consumers demonstrate a mix of premium and value-seeking behaviors. While affluent nationals opt for premium packages and international platforms, price sensitivity among expatriates has led to the popularity of freemium and ad-supported models. This duality is pushing content providers to adopt hybrid monetization strategies that blend subscription, pay-per-view, and advertising revenue streams

Competitive Landscape: Major Players and Strategies

The Qatar media ecosystem is defined by a mix of iconic national players and fast-growing digital innovators. Al Jazeera Media Network remains the most influential brand, reaching over 430 million households worldwide across its Arabic and English channels. Its digital-first approach, especially via Al Jazeera+, has resonated strongly with younger, global audiences, reinforcing Qatar’s soft power through journalism

BeIN Media Group, Qatar’s sports and entertainment powerhouse, commands massive subscriber bases across the Middle East and North Africa. With broadcasting rights for events like the UEFA Champions League and NBA, BeIN’s strategy hinges on exclusive content, regional licensing, and cross-platform accessibility. In early 2024, the company launched BeIN Originals, a content production division aimed at creating local drama series and documentaries

Meanwhile, Shahid, StarzPlay, and Netflix are aggressively expanding their Arabic-language libraries to cater to Gulf audiences. Netflix’s 2023 hit “Dubai Bling” featured Qatari influencers and was among the top 10 watched shows in the country that year, showing the appetite for culturally relevant yet globally polished content

Language and cultural sensitivity remain at the forefront. Platforms are increasingly dubbing or subtitling content in Arabic and integrating Islamic values into storylines—an approach welcomed by Qatari consumers. Additionally, Qatar Media City’s 2024 content fund has begun supporting local creators with grants, aiming to boost the number of Qatari media entrepreneurs by 200% by 2030

Author

Author:

Joseph Gomes Y (Head – Media and Entertainment)

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation. [Learn more]

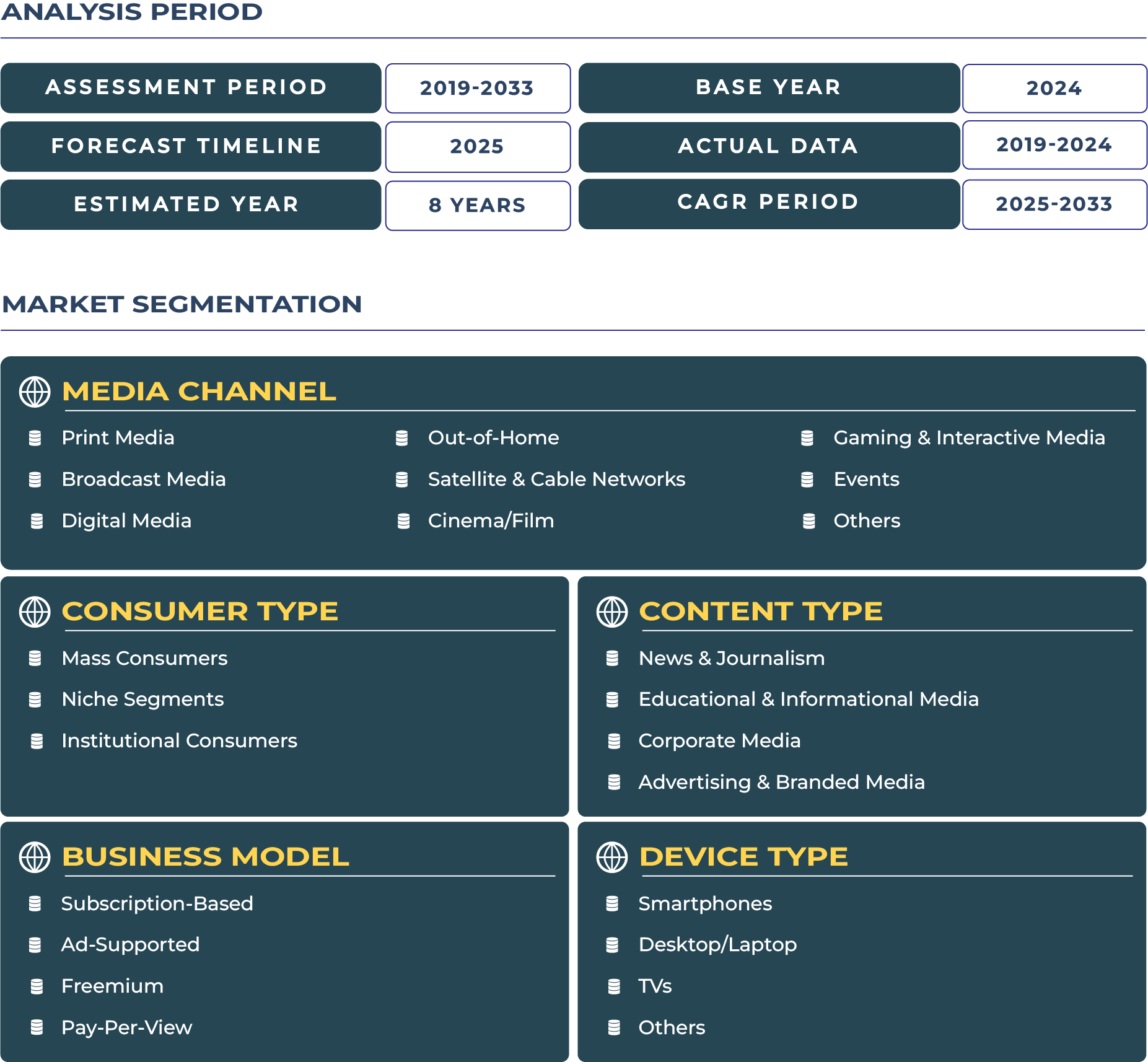

Qatar Media Market Segmentation

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

India Media Market Size | 2019-2033

- Report ID: MED511 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

South Africa Media Market Size | 2019-2033

- Report ID: MED5117 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

Brazil Media Market Size | 2019-2033

- Report ID: MED5135 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

Saudi Arabia Media Market Size | 2019-2033

- Report ID: MED5141 | Coverage: Country |

- Category: Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 | US$495 |

India Media Market Size | 2019-2033

- Report ID: MED511 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

South Africa Media Market Size | 2019-2033

- Report ID: MED5117 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

Brazil Media Market Size | 2019-2033

- Report ID: MED5135 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

Saudi Arabia Media Market Size | 2019-2033

- Report ID: MED5141 | Coverage:Country |

- Category:Media and Entertainment | Sub-Category: Media |

- Published Date: May 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe