Japan Media Market Size and Forecast by Media Channel, Content Type, Revenue Model, Consumer Type, and Device Type: 2019-2033

May 2025

| Format:

MARKET OUTLOOK

Japan Media Market Growth and Performance

- Revenue in the Japan media market amounts to USD XX.84 billion in 2025. The market is likely to grow annually by X.85% (CAGR 2025-2033).

- In the media industry in Japan, the XX device type market value is expected to stand at USD XX.81 billion by 2033.

Japan Media Industry Outlook

Evolving Dynamics: A 2024 Perspective

Japan media industry has long stood as a global cultural powerhouse, driven by an intricate balance of tradition and digital innovation. Valued at approximately USD XX billion in 2024, the Japan media market is undergoing a multifaceted transformation. The combination of high internet penetration (93%), robust smartphone ownership (86%), and increasing smart TV adoption (55%) has laid a strong foundation for content consumption. As the Japan media sector steps into the future, its trajectory is increasingly shaped by AI-driven personalization, augmented reality integrations, and the inclusion of an aging population into the digital mainstream.

The role of media within Japanese society remains deeply influential. Local content types such as anime and variety shows not only dominate domestic viewership but also fuel Japan’s media export revenues, which touched approximately USD 12 billion in 2023. This export strength is underpinned by robust IP franchises, notably from anime and J-dramas, which continue to expand globally via platforms like Crunchyroll and Netflix Japan. Meanwhile, the nation's high disposable income—around USD 30,500 per capita—supports sustained consumer spending on premium content across both OTT and traditional platforms.

Monetization Metrics: Paid Users, ARPU, and Market Health

At the core of the Japan media industry ecosystem lies a stable base of over 40 million OTT subscribers. With an average revenue per user (ARPU) of approximately USD 9 per month, platforms like Netflix Japan (7.3 million subscribers) and Amazon Prime (6.5 million) dominate, reflecting a preference for curated, high-quality content. What’s noteworthy is the contrast in monetization models between global and local services—AbemaTV, for instance, leverages a freemium model, attracting over 3.1 million users through free access to live news and entertainment before upselling premium tiers.

Media companies have also begun focusing more on cross-platform monetization. Sony Pictures Japan's partnership with Crunchyroll is a classic example, aimed at monetizing anime IPs across streaming, merchandise, and gaming. The key here is content localization and fan-driven ecosystem development, both of which are growing pillars of the Japanese digital content economy.

Cultural Preferences and Media Consumption Behavior

The Japanese consumer base is highly discerning. The average media consumption time stood at 6.4 hours per day in 2023, with a significant portion spent on anime, manga, and OTT content. More than 70% of streamed content is locally produced, emphasizing the dominance of homegrown entertainment. Urban consumers are increasingly drawn toward premium content, often preferring ad-free, on-demand services, while the older generation still leans towards free-to-air broadcasting, notably NHK and TV Tokyo.

Youth aged 15–34, comprising about 22% of the population, exhibit a deep affinity for creator-driven content and social media platforms like YouTube, TikTok, and Japan’s homegrown NicoNico. Monthly media expenditure in this demographic ranges between USD 17 and 28, driven by fandoms, livestream interactions, and anime exclusives. This hybrid consumption pattern is accelerating the convergence of mainstream and creator economies in the Japan media industry.

Governmental Catalysts and Strategic Brand Play

Japan's Ministry of Economy, Trade, and Industry (METI) has bolstered content innovation through the Cool Japan initiative, funding global media outreach with a fund worth approximately USD 450 million. Meanwhile, the Digital Agency is facilitating the digital transformation of public broadcasters, encouraging the blending of linear and digital formats.

Key players are adopting differentiated go-to-market strategies. NHK is deepening its global reach by streaming J-dramas internationally, leveraging public trust. Sony Pictures Japan is exploiting the global anime craze by co-producing with Crunchyroll. AbemaTV’s model of offering free live channels with premium on-demand options has proved effective in attracting urban youth. This multi-tiered approach reflects a shift from passive content delivery to immersive, user-centric ecosystems.

Conclusion: Towards a Hyper-Personalized, IP-Driven Future

The Japan media sector stands at a strategic inflection point. As ARPU stabilizes and consumer engagement deepens across multiple devices and formats, the industry's future will hinge on three key drivers: IP monetization, global export growth, and AI-enhanced personalization. In the race to capture audience loyalty, both local and international players are doubling down on cross-platform storytelling, creator partnerships, and culturally resonant content. Japan's continued media dominance will not just be defined by content quality but also by its agility in adapting to an increasingly interactive and immersive media landscape.

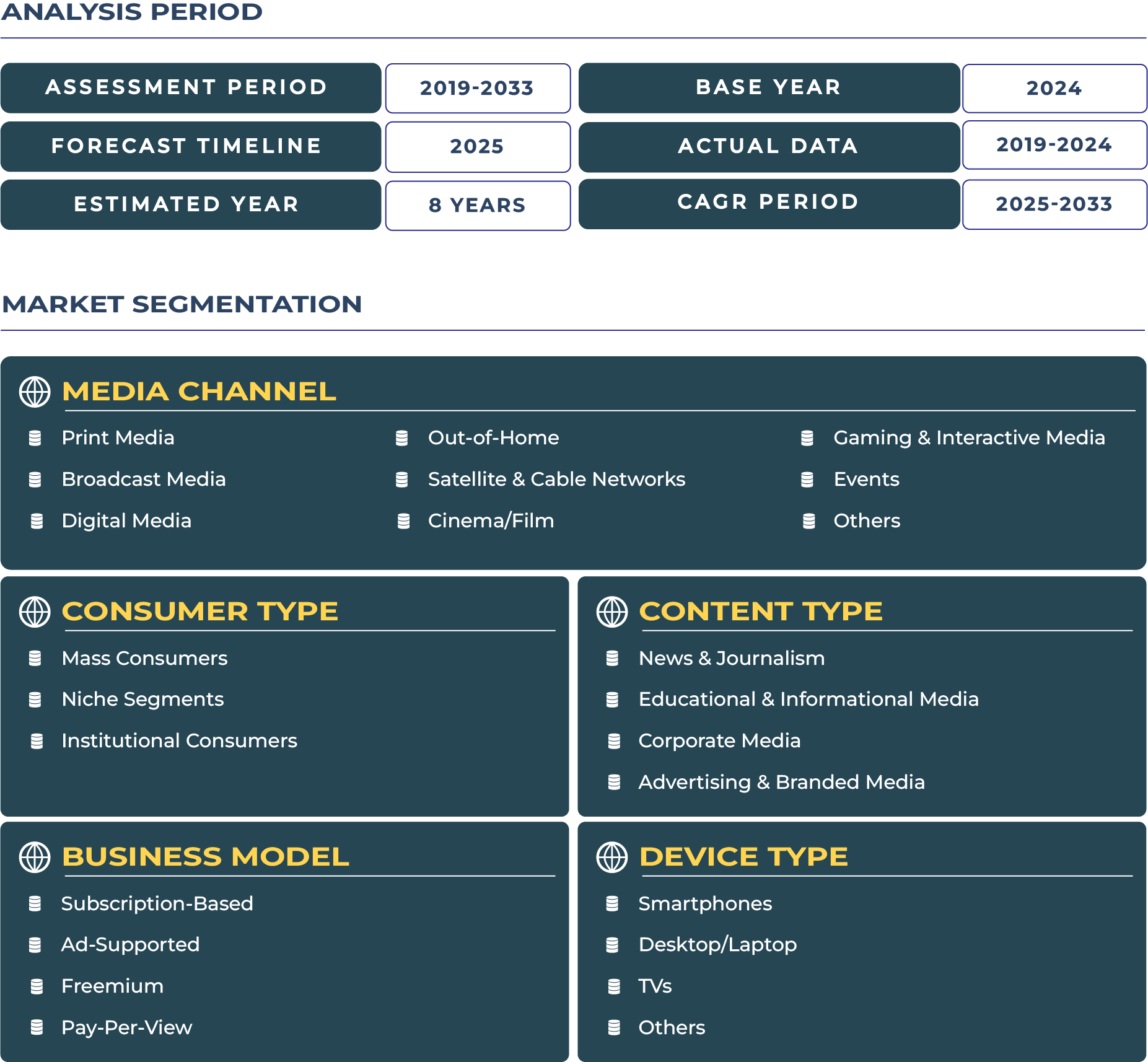

Japan Media Market Scope

*Research Methodology: This report is based on DataCube’s proprietary 3-stage forecasting model, combining primary research, secondary data triangulation, and expert validation.

[Learn more]

Related Reports

UK Public Cloud Market Size | 2019-2033

- Report ID: IT1811 | Coverage: Country |

- Category: Information Technology | Sub-Category: IT Software & Services |

- Published Date: Jul 2025 | US$495 |

Germany Public Cloud Market Size | 2019-2033

- Report ID: IT1812 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Jul 2025 | US$495 |

France Public Cloud Market Size | 2019-2033

- Report ID: IT1813 | Coverage: Country |

- Category: Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Jul 2025 | US$495 |

UK Public Cloud Market Size | 2019-2033

- Report ID: IT1811 | Coverage:Country |

- Category:Information Technology | Sub-Category: IT Software & Services |

- Published Date: Jul 2025 |US$495 |

Germany Public Cloud Market Size | 2019-2033

- Report ID: IT1812 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Jul 2025 |US$495 |

France Public Cloud Market Size | 2019-2033

- Report ID: IT1813 | Coverage:Country |

- Category:Information Technology | Sub-Category: Cloud Computing Technology |

- Published Date: Jul 2025 |US$495 |

Why Choose Us

24/5 Research Support

Get your queries resolved prior to and post purchasing research study

Customize As Per Specific Requirements

Get in-depth analysis based on your tailored research needs

Expertise in Tracking Niche Markets

Comprehensive view of latest technologies and opportunities across markets

360-Degree Analysis

Fact-based insights derived through supply & demand side analysis

Assured Quality

Deliver most accurate industry insights to maintain research quality

Information Security

Your confidential and personal data is secure and safe